Jane and her husband Joe stay within the midwest with their two teenaged youngsters and one parrot. Lately, Jane retired from her 24-year-long profession as a university professor and loves the brand new life-style she’s carving out for herself. Joe works from dwelling and the household enjoys spending plenty of time collectively.

Jane’s query at this juncture is whether or not or not she must return to full or part-time work at any level, or, if the couple can stay on Joe’s earnings alone till he too retires in 9 years. She’s additionally questioning if their asset allocation is suitable given their ages and projected retirement timeline.

What’s a Reader Case Examine?

Case Research tackle monetary and life dilemmas that readers of Frugalwoods ship in requesting recommendation. Then, we (that’d be me and YOU, pricey reader) learn by means of their state of affairs and supply recommendation, encouragement, perception and suggestions within the feedback part.

For an instance, take a look at the last case study. Case Research are up to date by members (on the finish of the put up) a number of months after the Case is featured. Go to this page for hyperlinks to all up to date Case Research.

Can I Be A Reader Case Examine?

There are 4 choices for people all for receiving a holistic Frugalwoods monetary session:

- Apply to be an on-the-blog Case Study subject here.

- Rent me for a private financial consultation here.

- Schedule an hourlong call with me here.

- Schedule a 30 minute call with me here.

→Unsure which option is best for you? Schedule a free 15-minute chat with me to study extra. Refer a buddy to me here.

Please be aware that area is proscribed for the entire above and most particularly for on-the-blog Case Research. I do my finest to accommodate everybody who applies, however there are a restricted variety of slots accessible every month.

The Purpose Of Reader Case Research

Reader Case Research spotlight a various vary of monetary conditions, ages, ethnicities, areas, objectives, careers, incomes, household compositions and extra!

The Case Examine sequence started in 2016 and, so far, there’ve been 98 Case Studies. I’ve featured of us with annual incomes starting from $17k to $200k+ and internet worths starting from -$300k to $2.9M+.

I’ve featured single, married, partnered, divorced, child-filled and child-free households. I’ve featured homosexual, straight, queer, bisexual and polyamorous folks. I’ve featured ladies, non-binary of us and males. I’ve featured transgender and cisgender folks. I’ve had cat folks and canine folks. I’ve featured of us from the US, Australia, Canada, England, South Africa, Spain, Finland, the Netherlands, Germany and France. I’ve featured folks with PhDs and folks with highschool diplomas. I’ve featured folks of their early 20’s and folks of their late 60’s. I’ve featured of us who stay on farms and folk who stay in New York Metropolis.

Reader Case Examine Tips

I most likely don’t have to say the next since you all are the kindest, most well mannered commenters on the web, however please be aware that Frugalwoods is a judgement-free zone the place we endeavor to assist each other, not condemn.

There’s no room for rudeness right here. The aim is to create a supportive setting the place all of us acknowledge we’re human, we’re flawed, however we select to be right here collectively, workshopping our cash and our lives with optimistic, proactive ideas and concepts.

And a disclaimer that I’m not a educated monetary skilled and I encourage folks to not make critical monetary choices primarily based solely on what one particular person on the web advises.

I encourage everybody to do their very own analysis to find out the most effective plan of action for his or her funds. I’m not a monetary advisor and I’m not your monetary advisor.

With that I’ll let Jane, in the present day’s Case Examine topic, take it from right here!

Jane’s Story

Hello Frugalwoods–thanks upfront in your recommendation! I’m Jane, a 50-year-old retiree/stay-at-home-parent who was lucky to have the ability to go away my profession as a university professor this previous 12 months. My partner and faculty sweetheart, Joe, works a distant company job. We stay a beautiful Midwestern existence with our two youngsters (one in highschool, one post-high faculty) and one parrot.

Hello Frugalwoods–thanks upfront in your recommendation! I’m Jane, a 50-year-old retiree/stay-at-home-parent who was lucky to have the ability to go away my profession as a university professor this previous 12 months. My partner and faculty sweetheart, Joe, works a distant company job. We stay a beautiful Midwestern existence with our two youngsters (one in highschool, one post-high faculty) and one parrot.

What feels most urgent proper now? What brings you to submit a Case Examine?

We’ve adopted the fundamental ideas of the FIRE (monetary independence, retire early) motion for a couple of decade now. We’re grateful to those that launched us to this motion and to content material creators like Frugalwoods who regularly educate us to problem societal norms relating to the definition of a “good life.” I felt assured leaving my profession final 12 months once we had been approaching “Coast FI” territory and it was clear my job was making it tough for me to be the most effective mother or father I might be to my youngsters, one in all whom has actually struggled.

Proper now, we’d like assist determining a plan for the following 10 years.

At that time, we are able to entry our retirement accounts and really feel comparatively assured with our capacity to navigate our personal funds. However earlier than then, a principal query is: when will I would like to hunt part- or full-time work, and the way a lot will I would like to herald?

What’s the most effective a part of your present life-style/routine?

I really feel “on high of” my life for the primary time. The home is clear, I’ve time to prepare dinner (which I LOVE) and take walks, and my stress degree is drastically decreased. I’m presently planning and beginning my vegetable backyard; I like to backyard and sit up for an ever-improving vegetable backyard annually. I’m additionally taking over some dwelling enchancment initiatives I’ve all the time wished to do and I’ve picked up a small quantity of volunteer work.

I get to be a stay-at-home-parent to my high-school-aged son and a greater help particular person to my 19-year-old daughter. Her stress degree, degree of functioning, and our relationship are markedly improved. I’m grateful that I can now give her the help she wants.

That is the primary time in our marriage that my partner’s profession has been prioritized over mine, and I really like watching him have this chance to develop. As a household unit, we spend most of our time collectively at dwelling, mountaineering, enjoying video games or benefiting from free leisure. I believe we spend way more time as a unit than most households with youngsters this age, and for that I’m grateful.

What’s the worst a part of your present life-style/routine?

I’ve had a tough time establishing a schedule that helps me really feel productive. My partner works from dwelling, my 19-year-old doesn’t drive and is a homebody, so there are often three of us in the home always. It generally seems like Groundhog Day. I used to be by no means an enormous spender, however as a result of I’m not bringing in an earnings, I really feel anxious about spending cash.

The place Jane Desires to be in Ten Years:

1) Funds:

1) Funds:

- Have good medical insurance.

- Perhaps working a part-time job that I like, however positively previous the accrual part of our lives.

- My husband want to cease working at age 60 (in 9 years) if potential. So much will depend upon our well being care state of affairs.

2) Life-style:

- I wish to be the place my youngsters are, and presumably within the higher Midwest the place my in-laws and husband’s household stay.

- Though we love our present home, I sit up for a smaller dwelling. Ideally, in 3 years we’ll downsize to a house that we are able to buy outright with the fairness we now have on this dwelling.

- Each youngsters out of the home with jobs and medical insurance.

- I desire a easy life; an enormous backyard, cooking most meals at dwelling, time with household.

- We prefer to journey some, however are good at utilizing factors and minimizing journey prices.

3) Profession:

- I don’t imagine I’ll ever re-enter academia. I might search a job that makes use of my tutorial experience in some unspecified time in the future sooner or later, but it surely might require further coaching. I’m undecided I’m all for doing that.

- I may additionally be completely happy working a part-time job right here and there, associated to my cooking/gardening/dwelling enchancment pursuits.

- I even have a number of concepts for small companies, however I don’t even know the place to start out with evaluating whether or not these are viable choices.

Jane and Joe’s Funds

Earnings

| Merchandise | Variety of paychecks per 12 months | Gross Earnings Per Pay Interval (whole BEFORE all deductions) |

Deductions Per Pay Interval (with quantities) | Web Earnings Per Pay Interval (whole AFTER all deductions are taken out, equivalent to healthcare, taxes, worker parking, 401k, and so on.) |

| Joe’s wage | 26 | $3,200 | $158 well being and dental; $290 401K contributions; $708 taxes | $2,044 |

| Joe’s added earnings as musician (approximate) | 1 | $2,500 | Taxes | $1,500 |

| Annual Gross whole: | $85,700 | Annual Web whole: | $54,644 |

Mortgage Particulars

| Merchandise | Excellent mortgage steadiness (whole quantity you continue to owe) |

Curiosity Charge | Mortgage Interval and Phrases | Fairness (quantity you’ve paid off) | Buy value and 12 months |

| Mortgage | $174,679 | 2.63% | 15-year fixed-rate mortgage | Zestimate – owed = $250K ($425K-$175K) | $325; bought in 2017 |

Money owed: $0

Property

| Merchandise | Quantity | Notes | Curiosity/kind of securities held/Inventory ticker | Title of financial institution/brokerage | Expense Ratio (applies to funding accounts) | Account Sort |

| Jane’s 403b | $822,488 | By way of the job I left; accessible with no penalty at age 55 if wanted. | 60% giant cap fairness index, 19% international fairness index, 16% small-mid fairness, 1% core bond index | Voya | .02%, .09%, .03%, .02% | Retirement |

| Joe’s 403b | $158,013 | Rolled over from earlier jobs | 100% FNILX | Constancy | 0% | Retirement |

| Joe’s Roth IRA | $88,137 | 100% FNILX | Constancy | 0% | Retirement | |

| Jane’s rollover IRA from a earlier job | $76,243 | 97% FZROX; 3% SPAXX | Constancy | 0% (FZROX) .1% (SPAXX) | Retirement | |

| Jane’s 457b | $69,473 | By way of the job I left; accessible now with no penalty | 70% Massive US Caps; 15% Small-Mid US Caps; 15% Non-US Shares | Empower | .01%, .01%, .05% | Retirement |

| Financial savings Account | $46,308 | Our “cushion” or Emergency Fund | 100% FDRXX | Constancy | 0.34% | Money |

| Joe’s 401K | $14,894 | Present job; he will probably be absolutely vested in August, and presently places in 5% with a 5% match | Prudential | Retirement | ||

| Jane’s Roth IRA | $13,900 | 100% FZROX | Constancy | 0% | Retirement | |

| Checking Account | $4,249 | Busey | Money | |||

| Whole: | $1,293,705 |

Automobiles

| Car make, mannequin, 12 months | Valued at | Mileage | Paid off? |

| Toyota Highlander 2010 | $8,700 | 210,000 | sure |

| Honda Match 2007 | $2,500 | 199,000 | sure |

| Whole: | $11,200 |

Bills

| Merchandise | Quantity | Notes |

| Mortgage with Escrow (together with insurance coverage) | $2,265 | approaching $1K in precept per 30 days |

| Groceries | $700 | contains family provides |

| Well being care prices (to get to deductible) | $400 | |

| Automotive bills | $375 | $200/mo for gasoline and $175 for upkeep or saving for brand spanking new automobile |

| Water/Sewer/Trash | $250 | Avg per 30 days. One thing is fallacious with our water payments; they’re exorbitant. We’re working to determine why. |

| Electrical (decreased price b/c partially photo voltaic) & Gasoline | $214 | avg per 30 days |

| Consuming out | $200 | |

| Son’s Sports activities Staff | $169 | month-to-month |

| Photo voltaic (photo voltaic sharing by means of NexAmp) | $155 | avg per 30 days |

| Journey | $150 | journey bills not lined by rewards factors; home journey this 12 months |

| Clothes | $120 | |

| Items and Holidays | $100 | |

| Auto insurance coverage (State Farm) | $75 | 2 drivers solely presently, will add one driver in June. Full protection on each automobiles. $900/12 months |

| Cell telephones (4 strains with Mint) | $65 | 4 strains with the MVNO Mint Mobile |

| Haircuts | $60 | minimize for Jane and Joe each different month, much less usually for teenagers, who put on their hair lengthy |

| Leisure | $50 | occasion tickets |

| sprinkler system | $19 | Month-to-month; activate and off as soon as per 12 months = $236 |

| Membership | $19 | botanical backyard ($225) |

| Pet bills | $18 | For the parrot |

| Subscription: Spotify | $10 | month-to-month |

| Month-to-month subtotal: | $5,414 | |

| Annual whole: | $64,965 |

Anticipated Social Safety

| Merchandise | Month-to-month Quantity | 12 months and age you’ll start taking SS |

| Joe’s anticipated Social Safety | $2,344 | at 67, in 2038 |

| Jane won’t be eligible for SS as a result of she didn’t pay in for most up-to-date job (20 yrs) and because of the Windfall Elimination Provision (WEP) | $0 | Notice that that is actually complicated to lots of people, however I’ve executed plenty of analysis on it and talked to the SSA, and I’m fairly assured that is true. It’s uncommon for college college to not pay into SS, however that was the case in my college system. I don’t know the precise quantity, however I’d must pay a considerable quantity into SS between now and retirement age to be able to not be topic to the WEP. |

| Annual whole: | $28,128 |

Credit score Card Technique

| Card Title | Rewards Sort? | Financial institution/card firm |

| Capital One Enterprise (Jane) | Journey | Capital One |

| Capital One Enterprise (Joe) | Journey | Capital One |

Jane’s Questions For You:

1) Once I left my profession, I felt assured in our aim to “coast FI”; my husband would proceed to work and I’d keep dwelling for no less than a 12 months after which work out what was subsequent. However that one-year mark will probably be upon us very quickly.

- How can I work out once I want to return to work and the way a lot I’d have to make?

- To what extent will my age and employment hole be an issue as my time away from work lengthens?

- Notice that I most likely can’t return to work full-time for no less than one other 12 months as my daughter wants extra time and a spotlight to get to a spot the place she’s thriving.

2) After finishing the worksheets for this Case Examine, I see some apparent locations for saving cash, however I’d love the readers’ concepts, too!

2) After finishing the worksheets for this Case Examine, I see some apparent locations for saving cash, however I’d love the readers’ concepts, too!

3) How does one start to discover self-employment?

- My concepts:

- Searching for out shoppers for whom I might prepare dinner (I already prepare dinner dinner each night time…why not prepare dinner the identical for an additional household or two?)

- Creating an internet site of homeschool-related content material

- Making an attempt to do some consulting associated to my tutorial areas of experience and… many different concepts!

4) How will we use what we find out about our monetary state of affairs to tell our selection of insurance policy?

- My husband has a ton of choices accessible by means of his employer and we went with the most affordable possibility that features an HSA as a result of I believed that’s what FIRE of us did.

- Nonetheless, I’m undecided that is the best selection as we’re not in a spot to make the most of the HSA as an funding automobile and we now have a very giant deductible.

5) What will we do with our “cushion” of money that we’re planning to make use of to complement my partner’s earnings for us to stay on?

- It’s presently not incomes any curiosity.

- Notice that the cushion serves as our Emergency Fund, and we now have two different locations from which we are able to draw with out penalty (my 457 and each of our Roth IRA’s–principal solely).

6) Ought to our retirement accounts be transferring away from equities, given our age? I understand there are various opinions on this, however I’d love to listen to yours and what the hive thoughts thinks.

Liz Frugalwoods’ Suggestions

I’m delighted to have Jane and Joe as in the present day’s Case Examine!

Jane’s Query #1: When do I would like to return to work and the way a lot do I have to earn?

This is dependent upon how a lot Jane and Joe need/have to spend each month. At current, their month-to-month spending outstrips their earnings; however, that’s one thing they may change in the event that they wished to. If Jane would favor not to return to work–and to as a substitute commit her time to her youngsters and probably pursuing self-employment–all they should do is convey their spending into alignment with Joe’s wage.

Present Annual Bills ($64,965) – Present Annual Earnings ($54,644) = $10,321 deficit

Let’s check out Jane and Joe’s bills to see if we are able to shut this hole. Anytime an individual needs to spend much less, I encourage them to outline all of their bills as Mounted, Reduceable or Discretionary:

- Mounted bills are stuff you can’t change. Examples: your mortgage and debt funds.

- Reduceable bills are essential for human survival, however you management how a lot you spend on them. Examples: groceries, utilities and gasoline for the automobile.

- Discretionary bills are issues that may be eradicated totally. Examples: journey, haircuts, consuming out.

To remain inside Joe’s wage, they’d have to restrict their spending to a most of $4,553.66 per 30 days. I categorized Jane and Joe’s bills and got here up with the under proposed plan of how they may accomplish this:

| Merchandise | Quantity | Notes | Class | Proposed New Quantity |

| Mortgage with Escrow (together with insurance coverage) | $2,265 | approaching $1K in precept per 30 days | Mounted | $2,265 |

| Groceries | $700 | contains family provides | Reduceable | $600 |

| Well being care prices (to get to deductible) | $400 | Mounted (I assume?) | $400 | |

| Automotive bills | $375 | $200/mo for gasoline and $175 for upkeep or saving for brand spanking new automobile | Reduceable | $275 |

| Water/Sewer/Trash | $250 | Avg per 30 days. One thing is fallacious with our water payments; they’re exorbitant. We’re working to determine why. | Reduceable | $175 |

| Electrical (decreased price b/c partially photo voltaic) & Gasoline | $214 | avg per 30 days | Reduceable | $200 |

| Consuming out | $200 | Discretionary | $50 | |

| Son’s Sports activities Staff | $169 | month-to-month | Discretionary | $169 |

| Photo voltaic (photo voltaic sharing by means of NexAmp) | $155 | avg per 30 days | Reduceable (I assume?) | $100 |

| Journey | $150 | journey bills not lined by rewards factors; home journey this 12 months | Discretionary | $25 |

| Clothes | $120 | Discretionary | $20 | |

| Items and Holidays | $100 | Discretionary | $10 | |

| Auto insurance coverage (State Farm) | $75 | 2 drivers solely presently, will add one driver in June. Full protection on each automobiles. $900/12 months | Reduceable | $75 |

| Cell telephones (4 strains with Mint) | $65 | 4 strains with the MVNO Mint Mobile | Mounted. Solution to go on utilizing a cheap MVNO!!!! | $65 |

| Haircuts | $60 | Lower for Jane and Joe each different month, much less usually for teenagers, who put on their hair lengthy | Discretionary | $10 |

| Leisure | $50 | occasion tickets | Discretionary | $10 |

| sprinkler system | $19 | Month-to-month; activate and off as soon as per 12 months = $236 | Mounted (I assume?) | $19 |

| Membership | $19 | botanical backyard ($225) | Discretionary | $19 |

| Pet bills | $18 | For the parrot | Mounted | $18 |

| Subscription: Spotify | $10 | month-to-month | Discretionary | $10 |

| Month-to-month subtotal: | $5,414 | Month-to-month subtotal: | $4,515 | |

| Annual whole: | $64,965 | Annual whole: | $54,180 |

Fortunately, Jane and Joe have comparatively low Mounted bills, which suggests it’s absolutely inside their energy to scale back the Reduceable and Discretionary gadgets to suit inside Joe’s take-home pay. Woohoo! Whether or not they wish to cut back/remove these things is completely as much as them, however it’s technically potential for them to stay on Joe’s wage alone–and to stay properly!

Moreover, Jane famous that they intend to downsize houses in ~3 years and probably purchase a smaller dwelling outright. That will be a significant game-changer since their greatest expense–by far–is their $2,265 mortgage fee.

Thus, it turns into a query of non-public choice and priorities:

- Would Jane somewhat return to work to be able to preserve their present spending degree?

- Would Jane somewhat cut back the household’s bills to be able to stay on Joe’s wage alone and thus not have to go ever again to work?

In fact there are additionally loads of in-between choices–equivalent to part-time work or partial expense reductions–that the household must also contemplate.

However Wait, This Finances Wouldn’t Embody Any Financial savings!

Properly, really it does as a result of Joe remains to be placing a pre-tax wage deduction into his 401k each pay interval! Woohoo once more! Jane and Joe have executed such an incredible job of saving and investing over time that they’ll be completely nice if they simply proceed Joe’s 401k contributions and spend the remainder of his wage. They’d basically be doing a kind of reverse model of Coast FIRE.

Properly, really it does as a result of Joe remains to be placing a pre-tax wage deduction into his 401k each pay interval! Woohoo once more! Jane and Joe have executed such an incredible job of saving and investing over time that they’ll be completely nice if they simply proceed Joe’s 401k contributions and spend the remainder of his wage. They’d basically be doing a kind of reverse model of Coast FIRE.

Let’s check out the remainder of their belongings to make sure they’ll be okay not saving something past Joe’s 401k contributions.

Asset Rundown

1) Money: $50,557

Between their two money accounts, the couple has $50,557 in money. Properly executed! The one draw back is that that is technically an overbalance of money. What do I imply by that? Isn’t additional cash all the time higher?!? Properly, yay and nay.

→The largest draw back to holding a lot cash in money is the chance value.

Having this a lot money solely is smart if:

- You plan to stop your jobs and never instantly discover one other;

- You might have main bills deliberate for the near-term, equivalent to: shopping for a home, shopping for a automobile, a big HOA evaluation, and so on.

Outdoors of those two situations, it turns into a large alternative value linked with the truth that your money is shedding worth day-after-day since it isn’t maintaining with inflation.

Whereas is can really feel instinctively “protected” to carry onto plenty of money, there’s a hazard to doing so. While you’re overbalanced on money, you’re lacking out on the potential funding returns you’d take pleasure in in case your cash was as a substitute invested in, for instance, the inventory market.

How A lot Ought to They Hold In Money?

Your money equals your emergency fund and your emergency fund is your buffer from debt:

- An emergency fund ought to cowl (at minimal) 3 to six months’ value of your spending.

- At Jane and Joe’s present month-to-month spend price of $5,414, they need to goal having an emergency fund of $16,242 to $32,484.

- In the event that they resolve to scale back their spending to stay on Joe’s wage, their emergency fund can commensurately cut back to someplace between $13,545 and $27,090.

All that being mentioned, if they might somewhat maintain this cash in money (and perceive the dangers to doing so), they will. Level right here is that they don’t want to avoid wasting up any additional cash, which is why I’m comfy suggesting the above finances that entails them spending all of Joe’s wage.

What To Do With This Money

No matter what the couple decides about Jane remaining retired, they should do one thing with this money that’ll leverage it in a roundabout way.

No matter what the couple decides about Jane remaining retired, they should do one thing with this money that’ll leverage it in a roundabout way.

→On the very, very least, they need to transfer this money right into a high-yield financial savings account that’ll earn them curiosity. There are a lot of accounts on the market providing nice rates of interest proper now.

For instance, as of this writing, the American Express Personal Savings account earns a whopping 3.90% in curiosity (affiliate hyperlink). Which means in a single 12 months, their $50,557 would earn $1,972 in curiosity!

Relying on what they resolve to do by way of Jane’s retirement, they will additionally contemplate quick to medium time period funding choices, equivalent to CDs, Cash Market Accounts, and Authorities Bonds. With all kinds of investments, you’re seeking to maximize your return, however make sure that the time horizon works in your plans. It’s type of like a ladder or hierarchy of choices:

- On the most accessible finish are high-yield financial savings accounts as a result of you may withdraw your cash at any time, in any quantity and with no penalty.

- In any case accessible finish are retirement investments as a result of it’s important to be age 59.5 earlier than you may withdraw your cash with out penalty.

- Within the center are quick and medium-term funding choices, which might make plenty of sense should you anticipate needing this cash in, say, three years to be able to purchase a brand new automobile.

2) Retirement: $1,243,148

Jane and Joe have a grand whole of $1.2M between their numerous retirement accounts, which is incredible.

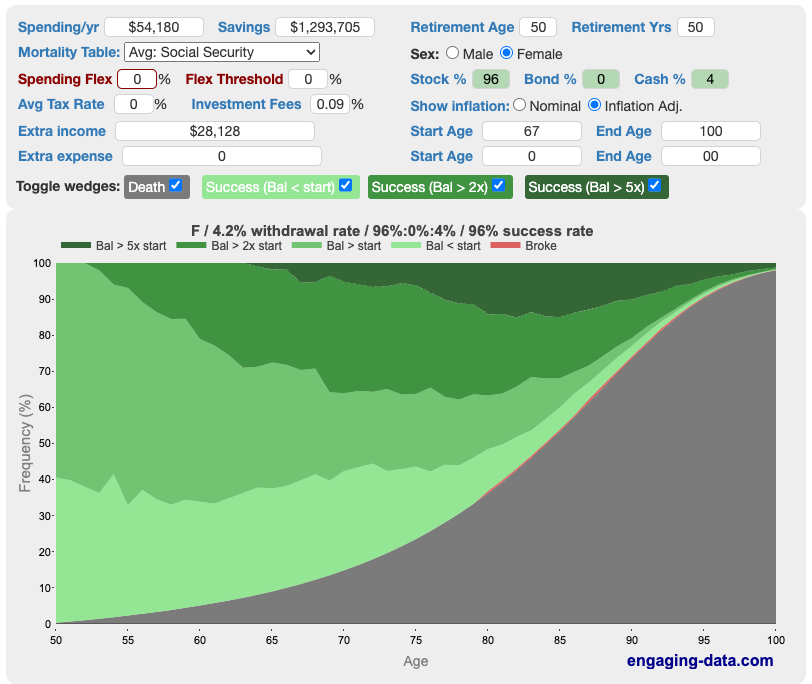

For enjoyable, I ran a calculation by means of Engaging Data’s Rich, Broke or Dead calculator to see what would occur if Joe additionally absolutely retired tomorrow:

What we see right here is that if Joe had been to affix Jane in retirement tomorrow, the couple has a 96% likelihood of success (in different phrases, of not working out of cash earlier than they die). That’s a reasonably good likelihood of success!

This success price relies on the variables of:

- Joe and Jane decreasing their annual spending to a most of $54,180.

- Each of them retiring at age 50 and dwelling to age 100

- Their present asset allocation of 96% shares and 4% money

- Joe starting to take Social Safety at age 67 at (an inflation-adjusted) $28,128 per 12 months

- Jane not receiving any Social Safety

- Neither of them working one other day of their lives

In mild of that, I’d say they’re in nice form! There are some caveats to this calculation, but it surely ought to give them the arrogance that they’ve loads of cash invested for retirement and that, in the event that they’re keen to scale back their spending, Jane doesn’t want to return to work (and neither does Joe!).

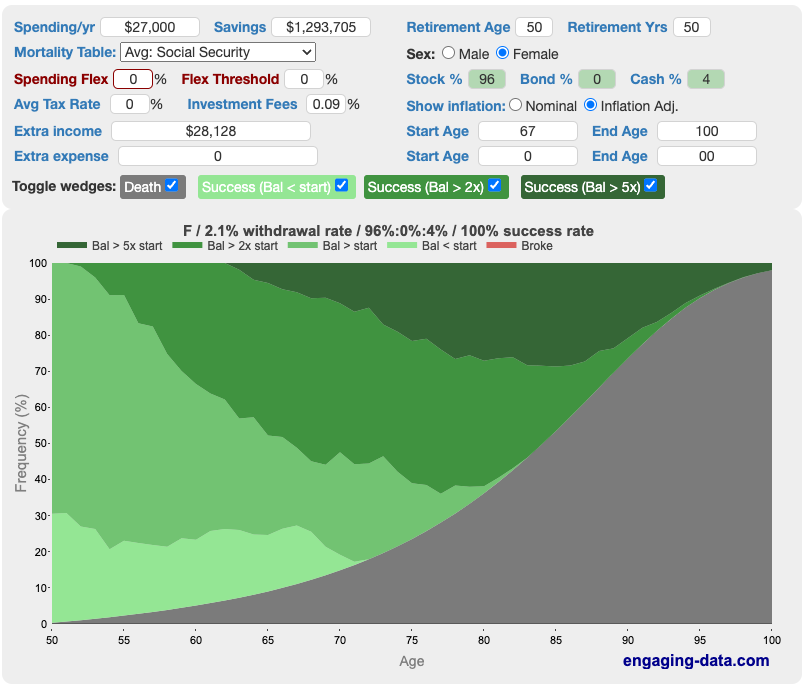

I’ll additionally level out that, in the event that they cut back their spending even additional–for instance after they draw back and remove their giant mortgage fee–their success price will increase to 100%:

-

- They presently spend 27180 yearly on their mortgage fee

- With out that, their annual spending might dip to a meagre $27,000!!!

Right here’s the chart:

However Wait, Isn’t Most of Their Cash Tied Up In Retirement Accounts?!?

Properly, sure and likewise no. Jane and Joe have a beautiful medley of accounts they usually’re all ruled by barely completely different guidelines.

1) Jane’s 457b: $69,473

In 457b plans, you’re allowed to withdraw cash penalty-free earlier than age 59.5, after you permit the employer who sponsors the plan. Therefore, if an individual plans to retire sooner than age 59.5, there’s an actual benefit to having a 457b. On account of this reality, this $69k might be spent by Jane and Joe at any time, with out penalty. In mild of that, from right here on out, they will contemplate this in the identical class as every other non-retirement (aka taxable) funding.

In 457b plans, you’re allowed to withdraw cash penalty-free earlier than age 59.5, after you permit the employer who sponsors the plan. Therefore, if an individual plans to retire sooner than age 59.5, there’s an actual benefit to having a 457b. On account of this reality, this $69k might be spent by Jane and Joe at any time, with out penalty. In mild of that, from right here on out, they will contemplate this in the identical class as every other non-retirement (aka taxable) funding.

Notice that you simply do pay taxes in your withdrawals, however that is often nice as a result of–presumably–by the point you’re withdrawing the cash, you’re retired and thus, your earnings and tax price are decrease.

2) Jane and Joe’s mixed Roth IRAs: $102,037

According to Charles Schwab, listed below are the principles for withdrawing previous to age 59.5:

You possibly can withdraw contributions you made to your Roth IRA anytime, tax- and penalty-free. Nonetheless, you could have to pay taxes and penalties on earnings in your Roth IRA.

Thus, Jane and Joe might withdraw the contributions they’ve made to their Roth IRAs, with out penalty, at any time.

3) Jane’s IRA: $76,243

If additional cash is required, Jane can contemplate a backdoor Roth IRA technique whereby you exchange a conventional IRA right into a Roth. This is usually a very excessive tax occasion, so tread fastidiously.

How Would This Work?

Based mostly on the low annual expense estimates above, this could carry them by means of to age 59.5, at which era they will start withdrawing from their 401k and 403bs with out penalties.

- Let’s say they anticipate Joe to retire till they’ve downsized and eradicated their mortgage fee, bringing their annual bills to $27k.

- They first spend down their extra $50,557 in money (above their emergency fund, which at that time would must be within the vary of $6,750 to $13,500, which leaves $37,057), which’ll cowl their bills for 1.37 years.

- Then, they start spending down Jane’s $69,473 457b, which’ll cowl their bills for an additional 2.57 years.

- We’re now at ~4 years, which suggests the couple is no less than 54 (probably older relying on when Joe retires).

- They’ll now have a look at withdrawing their contributions to their $178,280 in IRAs.

- And this quantity will really be much more since Jane ought to rollover her previous 403b (which has $822,488 in it) into an IRA.

→I wish to be clear that that is very “again of the envelope” math since we’re not taking plenty of variable components under consideration. However, I hope that this factors Jane and Joe in the best route for future analysis if that is one thing they wish to contemplate.

The Significance Of Diversifying Your Property

One thing I wish to spotlight is the dearth of diversification in Jane and Joe’s asset portfolio.

One thing I wish to spotlight is the dearth of diversification in Jane and Joe’s asset portfolio.

- They presently have all of their investments in retirement-specific automobiles.

- 100% of those are invested in equities (aside from 1% of Jane’s 403b in bonds)

Each of those are good issues to do–and to be clear, Jane and Joe have executed an A+ job of choosing funds with very low expense ratios!

Nonetheless, this falls underneath a “placing all your eggs in a single basket” funding strategy. As with most issues in life, diversification is an effective factor. The best and most easy means for them to diversify can be to place cash right into a taxable funding account, which is invested within the inventory market, however isn’t retirement-specific. With a taxable account, you’re not beholden to the principles governing retirement accounts.

In distinction to retirement automobiles (equivalent to 401k, 403bs, IRAs, and so on), taxable accounts:

- Haven’t any restrict on how a lot you may put into them

- Haven’t any restrictions on when you may withdraw the cash

- Are taxed (therefore their title)

- Since they’re not by means of an employer, you may make investments them in no matter you need (inventory, bonds, ETFs)

- Should not have any required minimal distributions (RMDs), which suggests you may go away your cash invested for so long as you need

→Since there are benefits and downsides to retirement and taxable accounts, it’s a good suggestion to have each.

They function in several methods and thus can serve you in several methods and completely different conditions. Forbes has this easy-to-understand article on taxable funding accounts should you’d prefer to study extra

When must you open a taxable funding accounts?

Should you’ve already:

- Paid off all high-interest debt

- Saved up a fully-funded emergency fund (held in a checking or financial savings account)

- Maxed out all potential retirement accounts

- Don’t want this money within the close to future for a significant buy (equivalent to a home)

Then… you may contemplate opening a taxable funding account!

I outlined above why you don’t wish to maintain huge quantities of money readily available, and our last Case Study detailed quick and medium-term investments to think about, equivalent to: CDs, Treasury Bonds and Cash Market Accounts. So in the present day, let’s speak about this different, longer-term funding possibility: the taxable account. I can really feel your enthusiasm already!!!

The place and How Do I Open A Taxable Funding Account?

Fortunately, you are able to do this by yourself by way of the world vast internet!

Fortunately, you are able to do this by yourself by way of the world vast internet!

- Select a brokerage:

- That is the place by means of which you make investments your cash. For instance: Constancy, Vanguard and Charles Schwab are all brokerages.

- If you have already got accounts (equivalent to your 401k) with a brokerage, it’ll be best to open a taxable funding account with them.

- Nonetheless, you wish to first make sure that the brokerage you choose presents low-fee funds.

- Select what you wish to make investments your cash in:

- Issues to think about when selecting what to put money into:

- Your danger tolerance. Investing within the inventory market is inherently dangerous. Would you be extra comfy with lower-risk, lower-reward choices, equivalent to bonds? Or higher-risk, higher-reward choices, equivalent to shares?

- Your age. How quickly are you anticipating withdrawing a proportion this cash? As mentioned on this Case Examine, many consultants contemplate 4% to be a protected price of withdrawal.

- The charges related to the funds you’re contemplating. Excessive charges (known as “expense ratios”) will eat away at your cash over time. DO NOT do this to your self! For reference, the next three brokerages and funds are thought of to be low-fee funding choices:

- Constancy’s Whole Market Index Fund (FSKAX) has an expense ratio of 0.015%

- Charles Schwab’s Whole Market Index Fund (SWTSX) has an expense ratio of 0.03%

- Vanguard’s Whole Market Index Fund (VTSAX) has an expense ratio of 0.04%

- Questioning methods to discover a fund’s expense ratio? Try the tutorial in this Case Study.

- Issues to think about when selecting what to put money into:

Ought to I put money into particular person shares or whole market index funds?

For me personally, I want a complete market, low-fee index fund that matches my asset allocation wants and danger tolerance. The reason being that, normally, investing in a complete market index fund offers you the broadest potential publicity to the inventory market (in addition to the bottom charges).

→In a complete market index fund, you’re basically invested in a teensy bit of each single firm within the inventory market, which provides you a ton of variety.

If one firm–and even one sector–tanks, your total portfolio isn’t toast. It’s the “not placing all your eggs in a single basket” model of investing. It’s what I do, it’s what the overwhelming majority of FIRE of us do and, better of all, it’s very, very simple to implement and preserve.

Along with whole market index funds, many people prefer to have a few of their portfolio in one thing like a complete bond ETF, as a result of bonds are a lower-risk (though additionally lower-reward) funding automobile.

Is it Smart to Put money into Particular person Shares?

In my view, completely not. Why? as a result of if that one firm goes down, your funding plummets. If Apple or Amazon or Netflix or whoever has a nasty quarter, you have a nasty quarter. In case you are as a substitute invested throughout the complete inventory market, firms can go bankrupt and your portfolio will nonetheless bob together with the broader inventory market. Investing in a person inventory is “placing all your eggs in a single basket.”

I contemplate investing in particular person shares to be a interest, not a monetary technique. Should you actually take pleasure in day buying and selling and wish to do it for enjoyable, go proper forward! However I wouldn’t do it with cash I would like. In my view, it’s not a lot safer than going to a on line casino.

When Ought to You Use Your Taxable Investments?

Ideally, you’ll maintain this cash invested till you retire. While you retire, you may start to drawdown a proportion of those funds annually to cowl your dwelling bills. As you close to retirement, you’ll wish to cut back the danger publicity of those investments so that you simply’re buffered from any main market downturns within the run-up to your retirement. Individuals solely “lose all of it” within the inventory market after they promote their shares at a loss and take successful.

Ideally, you’ll maintain this cash invested till you retire. While you retire, you may start to drawdown a proportion of those funds annually to cowl your dwelling bills. As you close to retirement, you’ll wish to cut back the danger publicity of those investments so that you simply’re buffered from any main market downturns within the run-up to your retirement. Individuals solely “lose all of it” within the inventory market after they promote their shares at a loss and take successful.

I understand this can be a lot to attempt to cowl in a single put up, so I extremely suggest the ebook, The Simple Path to Wealth: Your Road Map to Financial Independence And a Rich, Free Life, by: JL Collins, for anybody all for deepening their data round investing. It’s well-written and straightforward to know.

This leads us very properly (virtually like I deliberate it… ) into:

Jane’s Query #6: Ought to our retirement accounts be transferring away from equities, given our age? I understand there are various opinions on this, however I’d love to listen to yours and what the hive thoughts thinks.

Let’s start on the very starting

What’s An Fairness?

Equities, on this context, are the identical as shares. Should you personal shares/equities, you personal a chunk of an organization. As I famous above, shares are typically thought of to be extra aggressive, however extra rewarding. Conversely, bonds are thought of to be much less aggressive, however much less rewarding.

It’s like a sliding scale of danger vs. reward. You, the investor, must resolve the place you wish to be on this scale.

Portray with a VERY broad brush; normally:

- While you’re younger and have a few years earlier than retirement, you wish to be very aggressive in your investing. The thought being that you simply’ll be capable of trip out the inevitable ups and downs of the inventory market because it’ll be many many years earlier than you might want to withdraw any of this cash.

- Then, as you close to retirement, you wish to titrate your danger/aggression to make sure that you don’t lose cash if the market experiences a dip simply previous to your retirement.

HOWEVER, as with all issues, there are differing opinions on the knowledge of decreasing danger (and consequently reward) in a portfolio as you age.

Vanguard has this nice chart, which lets you search all of their funds in line with danger degree. As you’ll see, there are a selection of various bonds and cash market accounts one can select from.

Equally, Constancy has this very helpful site outlining their numerous funds by danger degree. It permits you to have a look at completely different constructions of funds in a pattern portfolio in line with their danger degree. As I famous above, diversification is sweet, which you’ll see mirrored in Constancy’s mannequin portfolios. Probably the most conservative portfolio they mannequin contains plenty of bonds and their most aggressive has all shares and no bonds. Then, there are a bunch of pattern portfolios in between.

What Ought to Jane Do?

I’ll reiterate that variety is an effective factor. I personally am not 100% in home index funds as a result of I prefer to play the sector. I’ve received some worldwide index funds (which you should buy proper by means of your useful, dandy brokerage), I’ve received some bonds, I’ve received all of it–even one solitary Bitcoin! The thought, right here once more, is to unfold out the danger and never rely solely on one supply or sector.

Rollover The Previous 403b

Jane must also look into rolling over her previous 403b into an IRA in order that she will be able to have full management over the funds she’s invested in.

Right here’s how to do this:

- Name the brokerage (or do it on-line) that presently holds the 403b to ask about doing a “direct rollover” into a conventional IRA at one other brokerage. Since Jane and Joe have already got plenty of accounts with Constancy, I assume that’s the place she’ll wish to put it.

- You’re possible not going to wish to roll this right into a Roth IRA since you’d then must pay taxes on the complete quantity all on this calendar 12 months (assuming that this 403b isn’t a Roth). If it’s a Roth, it may solely be rolled right into a Roth.

- The brand new brokerage (Constancy) will wish to know what you wish to make investments your rollover IRA in.

I like this text explaining rollovers: Your Guide to 401(k) and IRA Rollovers.

Abstract:

- Decide their high precedence:

- If Jane needs to stay retired, she completely can. The household can cut back their spending to permit them to stay simply on Joe’s wage.

- If Jane needs to return to work, she completely ought to.

- If Joe additionally needs to retire proper now, he might!

- On this occasion, the household would want to scale back their spending and likewise analysis a number of the retirement vehicle-to-cash conversions I outlined above.

- This math will get even simpler after they downsize and remove their giant mortgage fee.

- They’d additionally have to analysis what their state presents for medical insurance by means of the Reasonably priced Care Act. The ACA isn’t a boogeyman and it’s a completely nice method to get your medical insurance. It’s, in spite of everything, what I do for my household. The problem is that it’s ruled by every state and, as such, the prices and subsidies fluctuate wildly by state. They’ll analysis this by means of their state’s ACA web site.

- Look into diversifying their investments, probably to lower-risk, decrease reward avenues, equivalent to bonds. Additionally contemplate opening a taxable funding account to provide them extra flexibility.

- Resolve what to do with their monumental money cushion:

- If Joe needs to retire now, they may use this to cowl dwelling bills for awhile (and thus keep away from withdrawing something from their investments). In the event that they go this route, they need to transfer this cash right into a high-yield financial savings account in order that they’re no less than incomes curiosity on it.

- In the event that they don’t intend to make use of this cash within the close to future, they need to look right into a extra worthwhile possibility for the whole lot above their emergency fund, equivalent to:

- Opening a taxable funding account

- Opening a short-term funding automobile, equivalent to a CD

Okay Frugalwoods nation, what recommendation do you have got for Jane? We’ll each reply to feedback, so please be happy to ask questions!

Would you want your individual Case Examine to look right here on Frugalwoods? Apply to be an on-the-blog Case Study subject here. Rent me for a private financial consultation here. Schedule an hourlong or 30-minute call with me here, refer a buddy to me here, or e-mail me with questions (liz@frugalwoods.com).

By no means Miss A Story

Signal as much as get new Frugalwoods tales in your e-mail inbox.

{kind=link}